The current update on the lease accounting project is both the FASB and IASB staffs are drafting the new rules. There are still some small open issues and some due process steps but they expect the boards to issue a new rule by the end of this year. The transition date will likely be 2018 and that is the date when lessors and lessees will be required to apply the new rules. We have time, but there are things that you can be doing now to begin preparing for the future.

Leveraged Leases

There is good news and bad news when it comes to leveraged leases. Leveraged leases existing at the transition date will be grandfathered and that’s the good news. The bad news is that leveraged lease accounting will be dropped in the new rules. So after the transition date, a leveraged lease will be reported “gross” on a lessor’s balance sheet (the full lease asset and the leveraging debt will be shown on balance sheet). For big ticket lessors it is important to note that the leveraged lease accounting structure is used for the traditional leveraged tax leases of assets like aircraft and rail cars, but it is also used in real estate build-to-suit synthetic leveraged leases. It is the means to get the lessor’s accounting treatment of netting the non-recourse debt in a leveraged synthetic lease. If not for leveraged lease accounting, the gross lease investment and leveraging debt would be shown on the lessor’s balance sheet and returns on assets would be unacceptable.

So what should a lessor be doing now? I’d say invest in as many new leveraged tax and synthetic leases as you can up until the transition date. You can also actively trade leveraged leases as the classification of a lease does not change when sold to a new lessor (this rule should hold true even after transition, so the secondary market in leveraged leases should still exist).

After transition, netting of non-recourse debt on the balance sheet of the lessor in a new leveraged lease will not be allowed. For leveraged tax leases, alternative (although more complicated and requiring a partner, co-investor or co-lessor) partnership structures where you control 50% or less of the lessor entity such as a trust or Special Purpose Entity (SPE) will allow “net” presentation of your interest on your balance sheet. As lessor, you can use the equity method to account for your investment in the lease which means that for balance sheet presentation only the net investment in the leases is shown as the asset (the debt incurred by the partnership is not shown on the lessor’s balance sheet as it is netted against the leased assets to arrive at the lessor’s net investment in the lessor entity).

The issue with the loss of leveraged lease accounting for leveraged synthetic leases done after transition will be how to “sell down” an interest in a large deal. Partnership structures do not work for synthetic leases as they need an SPE, and FIN 46 would cause a synthetic lease with an SPE lease to be on balance sheet for the lessee. Under-leveraged lease accounting the leveraging debt is the means to reduce a lessor/arranger’s exposure. That is, the leveraging debt partially funds the deal, reduces the lessor’s risk and is netted against the lessor’s investment as it is off balance sheet. Also the leveraged lender is providing senior debt without taking any residual risk. Many lenders can’t or won’t take residual risk. When leveraged lease accounting goes away it will be difficult for an arranger or lessor to sell interests in the lease that are not treated as on balance sheet debt to the lessor. Under the proposed new rules one can still do the synthetic lease and buy residual insurance so that it is classified as a direct finance lease (DFL) which is a financial asset. One way to get a direct finance lease asset or a portion of it off the lessor’s balance sheet after transition will be to sell a “vertical” strip in the synthetic lease. For the transfer of a portion of a financial asset to be eligible for sale/off balance sheet accounting, that portion and the portion retained by the transferor must meet the definition of a participating interest. A participating interest is an interest in the entire asset, so one must “sell” an equal portion of the senior, subordinated and equity (residual) portions of a synthetic lease (hence the term “vertical” strip) to get sale treatment.

Sales-Type Leases

The changes to sales-type lease accounting are a bit convoluted to explain. Manufacturers and dealers who use third party involvement (residual insurance or guarantees) to achieve DFL/sales-type lease classification (that is to get the PV of payments and insured/guaranteed residual to equal 90% of the value of the equipment) will be impacted by changes in the rules. Those who do not need residual insurance or third party residual guarantees to achieve DFL/sales-type lease classification (this occurs in true leases where the lessor’s implicit rate is lower than the lessee’s incremental borrowing rate so that the PV of payments for the lessee is less than 90% of the equipment value while the PV for the lessor is 90% or more) will not see any change on sales-type lease accounting.

Current GAAP allows up front profit recognition for DFL/sales-type leases where the lessor has a gross profit as well as the recognition of lease/financing revenue over the lease term at a constant yield versus the lessor’s net investment in the lease. The current rules allow the lessor to include third party residual insurance or guarantees in the payments to be present valued to achieve the DFL/ sales-type classification. On the other hand, the proposed new rules are based on the idea that the sale evaluation involves only the terms of the lease between the seller/lessor and the lessee. So the lease will not be a sales-type lease if the lessor needs third party residual insurance or residual guarantees to meet the DFL classification tests, instead it will be a DFL with a high implicit rate used to recognize both the gross profit and finance revenue over the lease term. The implicit rate will be high as the PV in the implicit rate calculation is the cost basis not the list price of the equipment. The high implicit rate will offer a better revenue recognition pattern than if the lease is classified as an operating lease.

Under both current GAAP and the proposed new rules, lessor accounting for an operating lease with a gross profit element recognizes the gross profit through depreciating the cost basis (versus the list price) over the lease term so that the gross profit is recognized on a straight line basis over the lease term. Operating lease revenue is back ended with annual straight line recognition of rent income while the residual is recognized when the asset is remarketed through a sale or re lease.

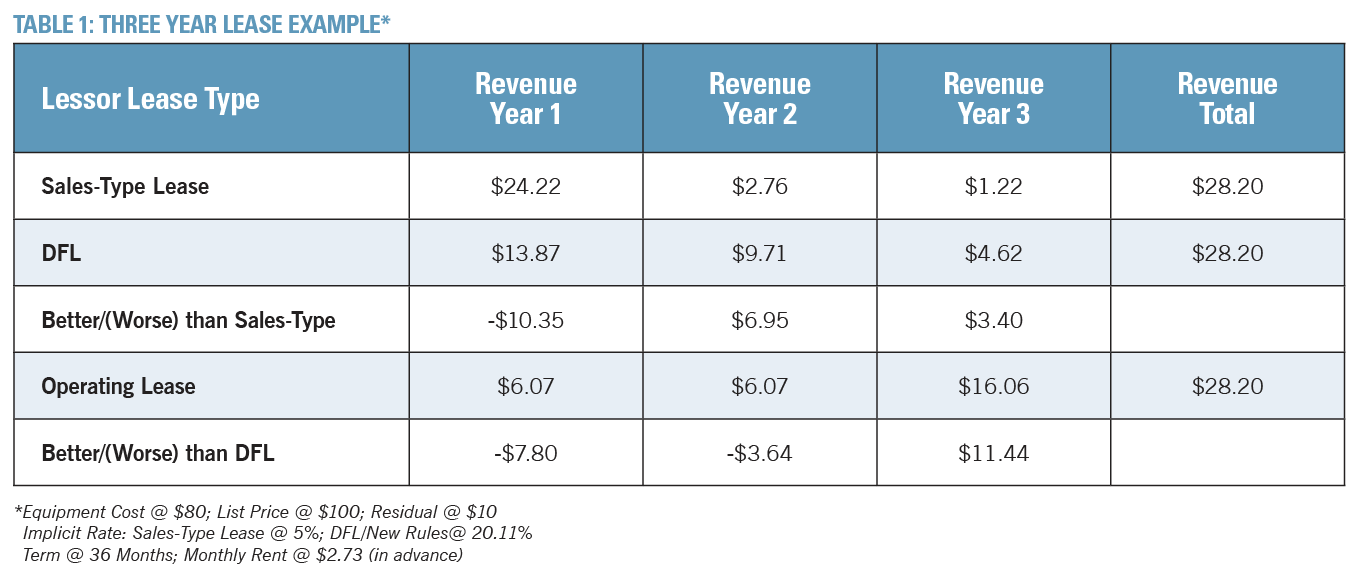

So where third party involvement is needed to achieve DFL treatment the lessor will have to analyze the costs and benefits of options to manage revenue recognition. Using a three-year lease example, Table 1 compares the impacts of today’s sales-type revenue pattern vs. still employing residual support and getting DFL treatment under the proposed rules vs. accepting operating lease accounting recognition.

The example above assumes a three-year term. It does not include the cost of residual insurance in the sales-type and DFL cases. The results will worsen the longer the lease term. The difference in timing of revenue disappears when the lessor reaches a “normalized” state where new business is equal each year. That point occurs at year three in the above example and matches the term of the lease in other examples. In other words, the negative pattern of earnings will go away over time, although with growth in volumes the issue never goes away. A lessor has to make its own analysis as to whether to buy residual insurance to accelerate revenue considering the cost of residual insurance and the tolerance to wait for the “normalized” state.

There is a time value to earnings meaning shareholders do place a value on when earnings occur. My former employer used its pretax cost of equity (assuming that is the timing preference rate a shareholder would use) to do a present valued return on assets calculation to make such decisions where the pattern of earnings was different in the alternative structures. The case with the highest present valued return on assets was the best choice. Given that the pretax cost of equity is high, typically the front ended options end up being the best choice.

Conclusion

There are some concerns for the leveraged lease segment and the sales-type lease segment but overall the industry should see little impact on new business volumes from the changes. In fact there are some opportunities. Stay ahead of the curve on the project by knowing the details and implications.

Bill Bosco is the Principal of Leasing 101, a lease consulting company. Bosco has more than 40 years of experience in the leasing industry. His areas of expertise are accounting, tax, financial analysis, structuring, pricing and training. He has been on the ELFA accounting committee since 1988 and was chairman for 10 years. He is a frequent author and speaker on leasing topics. He has been selected to the FASB/IASB Lease Project working group as a representative of the ELFA. He can be reached at [email protected], www.leasing-101.com or 914-522-3233.