1. Residual — Collateral Value Risk

During the recession, business aircraft owners experienced a “frightening downward spiral” of residual/collateral values according to a 2013 study titled: “Business Aircraft — Gaining Altitude From Recession to Recovery: Aircraft Transactions Build Momentum Despite Industry Challenges,” written by David G. Mayer, a co-author of this article. The recession changed deal approvals to a more highly controlled process under new regulations and strengthened company policies.

As a result, residual/collateral value concerns trigger complex negotiation of lease and loan provisions covering maintenance, return conditions (leases) and limitations on utilization of the aircraft. Also, astute sellers/buyers of pre-owned aircraft heavily negotiate purchase price, inspection process and repair risk regarding “discrepancies.” These elements require interdisciplinary collaboration of business, aviation, tax, legal and risk management experts.

2. State Sales and Use Taxes

Most transaction parties look for the “fly-away” exemptions from sales tax at the title transfer location, but do not always address the “mirror image” use taxes at the aircraft’s home base that applies in many jurisdictions. It is essential to do both when planning for state sales and use tax obligations.

It is naïve to take a “catch me if you can” attitude for those who believe fly-away exemptions mean zero sale/use taxes liability at home. States now search the Internet and the Federal Aviation Administration (FAA) registry to snag out-of-state purchasers to pay sales or use taxes. They may refuse to give errant taxpayers the benefit of the doubt for submitting sloppy or late paperwork. States may even apply collection pressure to raise tax revenue even if they do not stand on solid legal authority (e.g., Texas) for taxation. Knowing the ropes may save the hanging.

3. Compliance with FAA Operating Rules

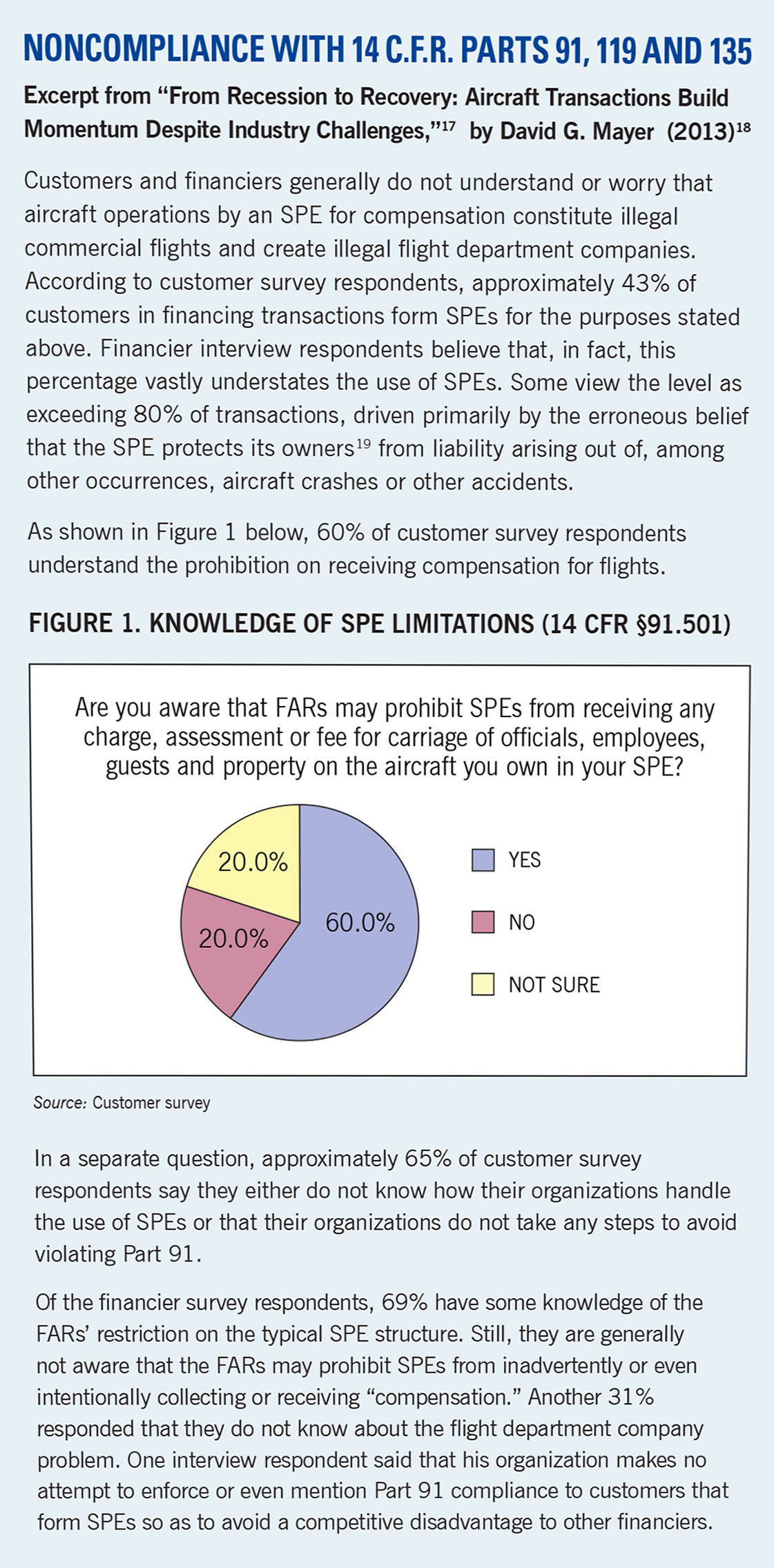

Operators must juggle their operations and other obligations (e.g., Federal and state taxes) to avoid violations of FAA operating rules. One frequent violation of the Federal Aviation Regulations (FARs) stems from using a special purpose entity, such as a limited liability company (SPE), to operate a private aircraft. SPEs cannot “hold out” (i.e., market to the public) or, as more often happens, operate for the benefit of their owners or members, which the FAA considers to be operation for “compensation or hire.” If they fail to devise a compliant structure under Part 91 (private operation), with limited exceptions, the FAA can say they conduct “commercial operations” as an illegal “flight department company.” According to the study, 60% to 80% of operators violate these rules which squarely fall under the FAA’s regulatory oversight and power to impose potentially serious financial penalties (e.g., $25,000 per violation).

Most financiers should approve structures and documentation designed to comply with the FARs, such as the SPE entering into an operating agreement or a lease with the lawful operator. Ironically, absent such approval, financiers may close their deals with customers in default and exposed immediately to FAA regulatory enforcement actions. The parties should, therefore, document agreed structures before or promptly after financial closing.

4. Federal Excise Taxes

The Internal Revenue Service (IRS) has expanded its assessments of Federal Excise Tax (FET) on Part 91 management agreement payments. This action arises, in part, due to a 2012 Chief Counsel Advice (CCA) that purportedly justifies charging FET. Even though the National Business Aviation Association has successfully persuaded the IRS to stop certain audits and re-study by this CCA analysis, the IRS auditors can still assess FET where they believe the management company has “possession, command and control” of an aircraft. The key is to structure non-commercial transactions taking into account the CCA and other FET principles.

5. Non-Citizen Trusts

Only a “citizen of the United States” can register an aircraft at the FAA. However, non-U.S. citizens (NCs) can register indirectly by forming and beneficially owning non-citizen trusts (NCTs). The owner trustee, which is a U.S. citizen, holds legal title. It can, therefore, register the aircraft on behalf of NCs.

As of September 16, 2013, NCTs (as contrasted with voting trusts) must comply with a “policy clarification” issued by the FAA on June 18, 2013. The NCT clarification alters transaction structuring and filing at the FAA civil aircraft registry. It also imposes information gathering/turnover duties on owner trustees. Accordingly, the parties will likely encounter, at least in the near term, more extensive diligence, analysis, negotiation and documentation to satisfy the new NCT rules.

Conclusion

Purchasing and financing private aircraft triggers many intersecting and complex legal and business issues. Five of the hottest points listed above can change rapidly, but undeniably, these often spool up in private aircraft transactions.

David G. Mayer is a partner at Shackelford, Melton & McKinley. He is the author of Business Leasing for Dummies and the founder of Business Leasing and Finance News, an online newsletter published for a decade. He is known for his work in domestic and international business aviation matters as well as for his extensive equipment financing/leasing transaction experience. He can be contacted at [email protected].

David T. Norton is a partner at Shackelford, Melton & McKinley. An active pilot and Certified Flight Instructor, he is known nationally for his regulatory and transactional work in the business aviation law arena, most recently completing service as the co-chair of the joint FAA/Industry RVSM LOA Process Enhancement Team of the FAA’s Performance-Based Advisory Rule Making Committee. He has an extensive background in tax, risk management and regulatory matters for private aircraft. He can be contacted at [email protected].

For the complete list of endnotes, please click here.

No tags available