Patrick Trammell,

Principal ,

Southeastern Commercial Finance

Commercial lenders will face many new and unique challenges over the coming months as the full effects of the coronavirus pandemic are felt throughout the economy. For commercial customers, cash flow, liquidity and credit tightening dramatically across industries is the new normal. In these uncertain times, no segment of the bank commercial portfolio is under as much short and long-term risk as the Commercial and Industrial (C&I) line of credit segment.

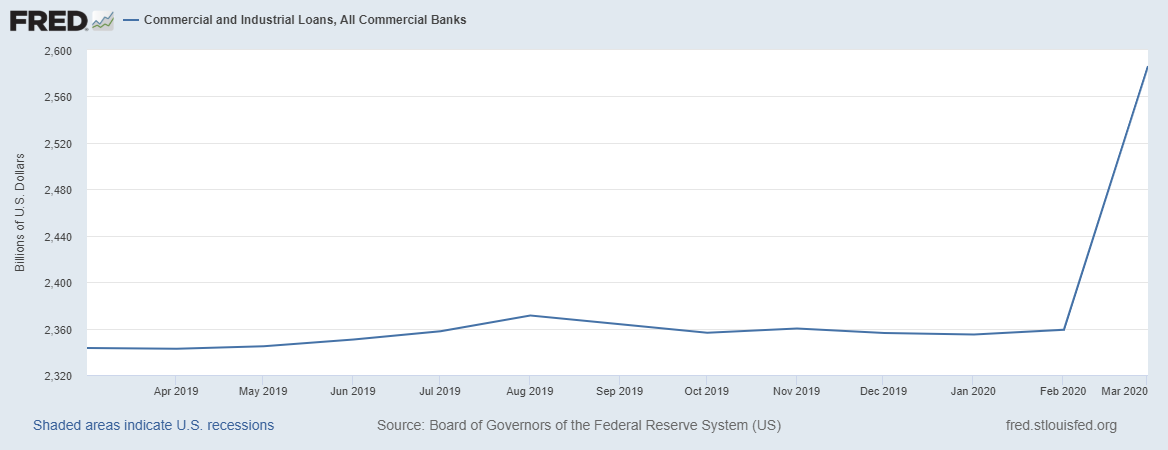

According to the Federal Reserve, beginning in mid-March, C&I loans surged at the highest rate in 73 years. The week of March 27 saw a $200 billion spike in that week alone. Clearly, this indicates commercial borrowers drawing down excess borrowing capacity to build cash reserves.

The nearest phenomenon to this borrower behavior was the great recession of 2008, however there are important differences. The great recession was caused by an asset bubble in the financial markets. The pandemic is a full-blown economic recession which creates dynamics specific to C&I credit risk:

Evolving Risk Profiles Indicate Need for Enhanced Oversight

The standard C&I bank line of credit is generally monitored by a monthly borrowing base certificate and governed by standard financial covenants, such as fixed charge coverage, debt to worth, guarantor liquidity and material adverse change provisions. For many years, C&I Credit Professionals have used some variation of the following characteristics to delineate monthly reporting from more intensive oversight:

In a normal economic environment, this level of oversight of the C&I line is an appropriate part of “managing the relationship.”

Federal Reserve statistics indicate significant increases in borrowings at the same time that revenues are declining at alarming rates. This would indicate that “robust excess line of credit availability” is certain to evaporate for many bank borrowers. Early statistics show similar erosion in covenant compliance and profitability as well.

To prepare and respond to the issues listed above, lenders and credit professionals should consider implementing plans with their C&I borrowers, which both protect their current loan position and anticipate borrower needs in the short, intermediate and long term. C&I lending requires a continually open, honest and transparent business relationship between the lender and the borrower. Depending on the structure of the loan, the lender may have monthly, weekly, or even daily discussions with the borrower about draws, repayment plans and current business issues.

Lenders and credit professionals should immediately consider analyzing and stress testing at the customer level in as much detail as possible by performing the following actions:

Risk Level Structure and Reporting Adjustments

Changing economic conditions might very well create the necessity for adjustments in structure of existing C&I facilities. Characteristics which might indicate the appropriateness of tighter controls include the following:

In the case of one or more of the above noted signs of C&I loan deterioration, tighter controls may be employed to protect the lender’s position and assist borrowers in more intensive focus on cash management. These tighter controls may include:

In uncertain and contracting economic times, the level of oversight of the C&I line must necessarily be adjusted from “managing the relationship” to more intensively “managing the line of credit.”

Keys to Success

By all accounts, the pandemic crisis and its effects on the economy will be deep and extended. Perhaps no segment of the financial markets is more at risk for commercial banks than the C&I segment. These times will require clear thinking, purposeful decision making, planning and execution. Clear and consistent communication between lenders and borrowers is imperative to allow bankers to protect their institution’s balance sheets while providing borrowers the best opportunity to weather this downturn. There is much that is out of the control of the most diligent bankers and the best business people. There is, however, much within the control of both. Experienced bankers don’t have crystal balls, but by communicating effectively and adhering to best practices, they can help both their institution and valuable customers in navigating this process.

Patrick Trammell is a principal of Southeastern Commercial Finance, LLC. He has written and lectured on C&I and asset based lending topics both nationally and internationally.

No categories available

3 Replies to “Managing C&I Risk in a Time of Pandemic”

Pat,

Thank you for an excellent summary.

C&I loan officers will once again need to revert to the basics:

Knowing their customers well

Encouraging transparency

Shortening reporting schedules to properly react to an ever changing environment.

This crisis will determine, in short order, the professional from the casual participants.

The industry will reward those professionals who are able to calmly perform during this crisis. I am relatively confident that there are enough great lenders to help the banking industry navigate the coming months.

Thank you so much for your comment Scott. Very well said, you got to the point better than I did. It’s simple and fundamental. We’ll see who remembers that this cycle. Best to you and your family.

Pat this is great.

One problem that’s hitting today is that nearly every borrower needs the lender’s attention. While the lender does need to spend more time in the fundamentals and should require more frequent financial reporting, there simply aren’t enough hours in the day.

Technologies like what we’ve built at Fincura can help lenders sift through these piles of data and still get home in time for dinner!