Cerebro Capital, a commercial loan platform, released its new quarterly survey on non-bank lending for middle-market commercial and industrial (C&I) loans. The results illustrate the perspectives of private credit lenders, also known as alternative lenders or non-bank lending institutions.

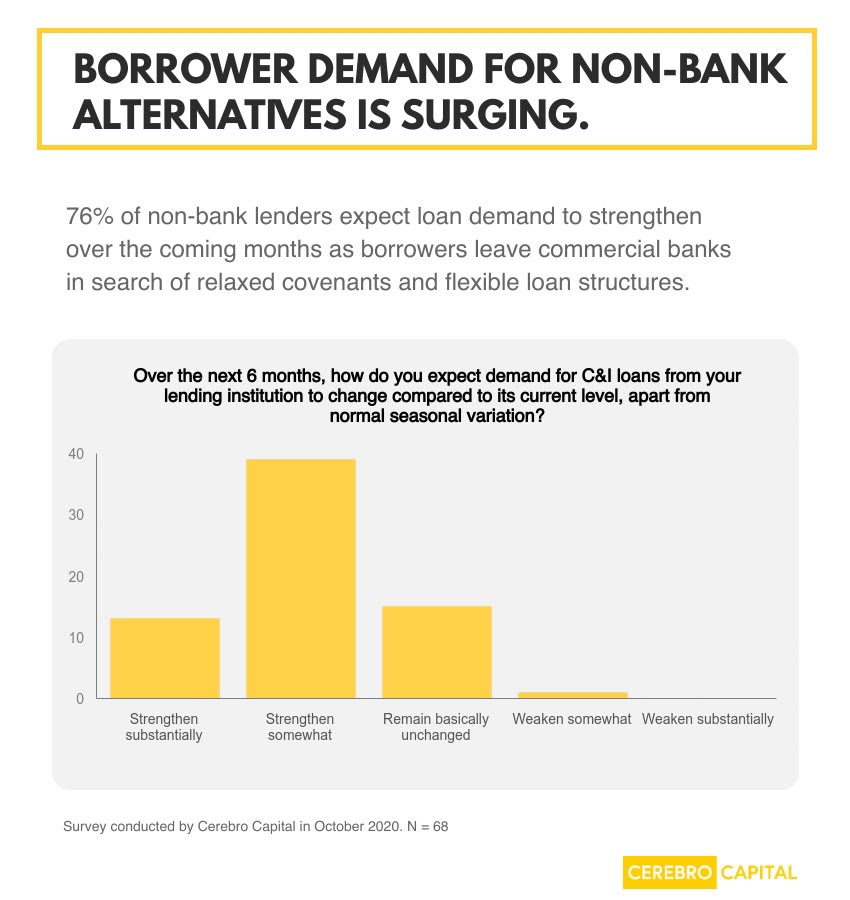

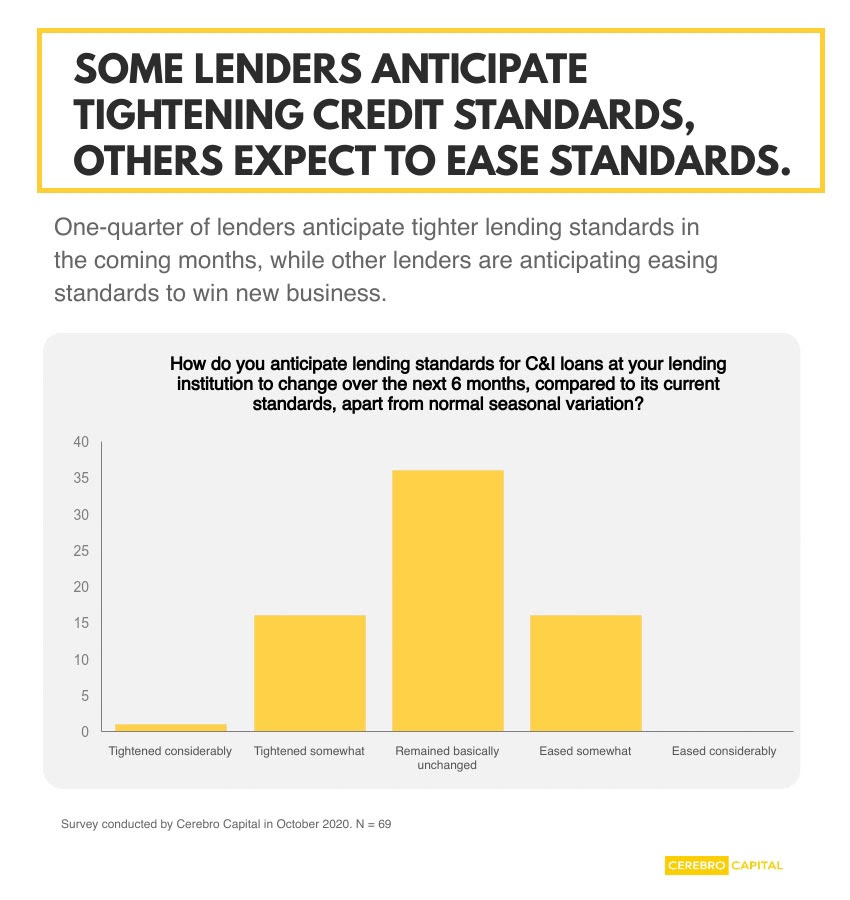

Non-bank lenders are changing credit standards in response to economic volatility, with 49% of respondents indicating that credit standards for C&I loans tightened during Q3/20. At the same time, 76% of non-bank lenders expect loan demand to surge over the coming months as borrowers leave commercial banks in search of relaxed covenants and flexible loan structures.

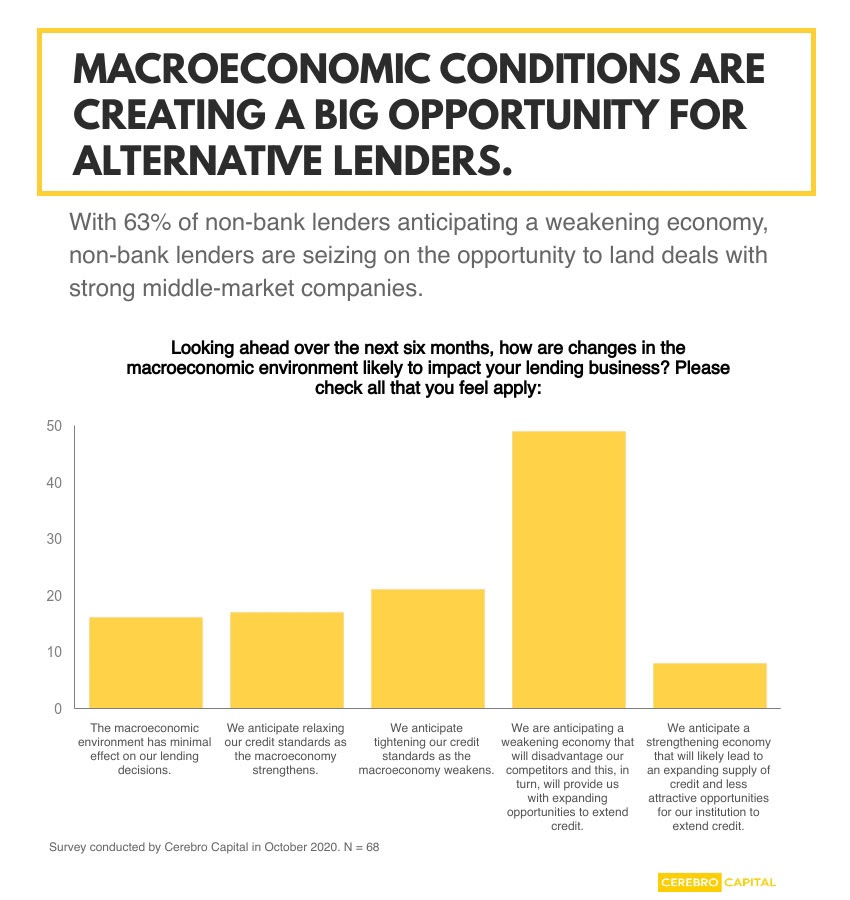

Several key findings in Cerebro’s survey indicate that non-bank lending institutions are continuing to strengthen their foothold in the private debt markets and will be a key resource for middle market companies as they explore financing options through 2021. With 63% of non-bank lenders anticipating a weakening economy that will disadvantage competitors and provide more opportunities for them to lend, non-bank lenders are seizing the opportunity to land deals with strong middle market companies. In fact, more than one third of non-bank lenders reported that they have already lowered rates for high-quality borrowers.

Additionally, 35% of non-bank lenders indicated that there is increased demand for draws on existing loans or lines of credit, providing more opportunities to extend their relationships with existing borrowers. In a similar question asked by the Federal Reserve’s Senior Loan Officer Quarterly Opinion Survey, only 17% of bank lenders are seeing increased demand for draws.

The survey included non-bank lending partners nationally and was conducted by Cerebro as a complement to the Fed’s survey on bank lending practices. While commercial bank lending has been tracked for the past 25 years, non-bank lending credit markets are not studied as consistently despite the market’s growth, according to Cerebro. Non-bank lending institutions are forecasted to hold $1 trillion of loan commitments by the end of 2020, up from $300 billion in 2010, according to the Alternative Credit Council. Non-bank lending is now one third of the size of bank lending to middle market companies in the United States.

Non-bank lenders from Cerebro’s lender network were surveyed in October 2020 and lender participation exceeded the number of participants in the Fed’s Senior Loan Officer Survey in the same period by 10%, according to Cerebro. Participating lenders represented more than $335 billion in combined assets managed, with a primary lending focus of loan sizes from $2 million to $100 million.

“Non-bank lending institutions have grown rapidly since 2008, after commercial bank lending was severely constrained,” Kevin Gaughan, director of lender relations at Cerebro Capital, said. “As the non-bank credit market has grown, loan terms have lowered interest rates and fees in an effort to win high quality corporate borrowers away from commercial banks and competitors.”

The array of debt financing options has helped address unmet borrower needs and brought borrowing opportunity to middle market companies seeking loans between $2 million and $100 million. Cerebro has seen non-bank lenders offer their most aggressive structures with minimal covenants in loan requests from sponsor-backed companies, or from non-sponsored borrowers with EBITDA above $3 million. Companies experiencing either high growth or unexpected deterioration can benefit from relaxed covenants, interest-only periods and collateral-lite structures that are common in non-bank loan structures.

More than half of the more than 800 lenders on Cerebro’s platform are non-bank institutions. Cerebro offers middle-market companies a data-driven approach to navigating hundreds of non-bank lenders, which have more variation in underwriting criteria than commercial banks. The diversity of non-bank lenders on Cerebro’s lender network includes mezzanine funds, business development companies and venture debt lenders.

“Top middle market CFOs should be regularly evaluating the expanding universe of corporate lenders, especially in times of economic volatility,” Matthew Bjonerud, CEO of Cerebro Capital, said. “A recession or a sudden economic shock like COVID-19 can result in many companies switching lending partners. Wise management teams know that larger and more flexible loans can be a huge competitive advantage and those loans can be easier to source in the non-bank market.”

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com