According to International Data Corporation’s Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, spending on compute and storage infrastructure products for cloud infrastructure, including dedicated and shared environments, decreased 2.4% year over year in Q2/21 to $16.8 billion. This decrease came after six quarters of year-over-year growth and most notably compares with the 39.1% annual growth in the market in Q2/20 near the beginning of the COVID-19 pandemic when the first wave of business and country closures caused a spike in investments in cloud services and infrastructure. Investments in non-cloud infrastructure increased 3.4% year over year in Q2/21 to $13.4 billion, recovering from a 7.2% decline in Q2/20.

During Q2/21, spending on shared cloud infrastructure reached $11.9 billion, a decrease of 6.1% compared with Q2/20 and a 17% increase from Q1/21. This weakness in year-over-year demand from public cloud service providers came after an exceptionally strong Q2/20 in which spending increased 55.5%, driven by the spike in demand for cloud services in the first months of the pandemic. Such a discrepancy in growth rates attributable to unexpected events creates “hard” comparisons that don’t reflect long-term trends, according to IDC, which expects to see continuously strong demand for shared cloud infrastructure, with shared cloud infrastructure spending surpassing non-cloud infrastructure spending by 2022. Spending on dedicated cloud infrastructure increased 7.8% year over year in Q2/21 to $4.9 billion, with 46.5% of this amount deployed on customer premises. IDC expects that cloud environments will continue to outpace non-cloud throughout its forecast.

Despite weakness in Q2/21, IDC is forecasting cloud infrastructure spending to grow 12% to $74.3 billion for 2021, while non-cloud infrastructure is expected to grow 2.7% to $58.9 billion after two years of declines. Shared cloud infrastructure is expected to grow by 11.1% year over year to $51.4 billion for the full year. Spending on dedicated cloud infrastructure is expected to grow 14.1% to $22.8 billion for the full year.

As part of its tracker, IDC monitors various categories of service providers and how much compute and storage infrastructure they purchase, including both cloud and non-cloud infrastructure. The service provider category includes cloud service providers, digital service providers, communications service providers and managed service providers. In Q2/21, service providers as a group spent $17.1 billion on compute and storage infrastructure, down 1.9% from Q2/20 and up 13.6% from Q1/21. This spending accounted for 56.5% of the total compute and storage infrastructure market. IDC expects compute and storage spending by service providers to reach $74.6 billion for 2021, growing at 10.5% year over year.

At the regional level, the year-over-year changes in spending on cloud infrastructure were mixed: Spending increased across the Asia/Pacific subregions as well as in Latin America, Canada and central and eastern Europe and declined in the United States, western Europe and the Middle East and Africa. Canada experienced the strongest year-over-year increase in cloud infrastructure spending in Q2/21 at 25.6%, while western Europe recorded the strongest decline at 8.8%. For the full year, spending on cloud infrastructure is expected to increase across all regions compared with 2020.

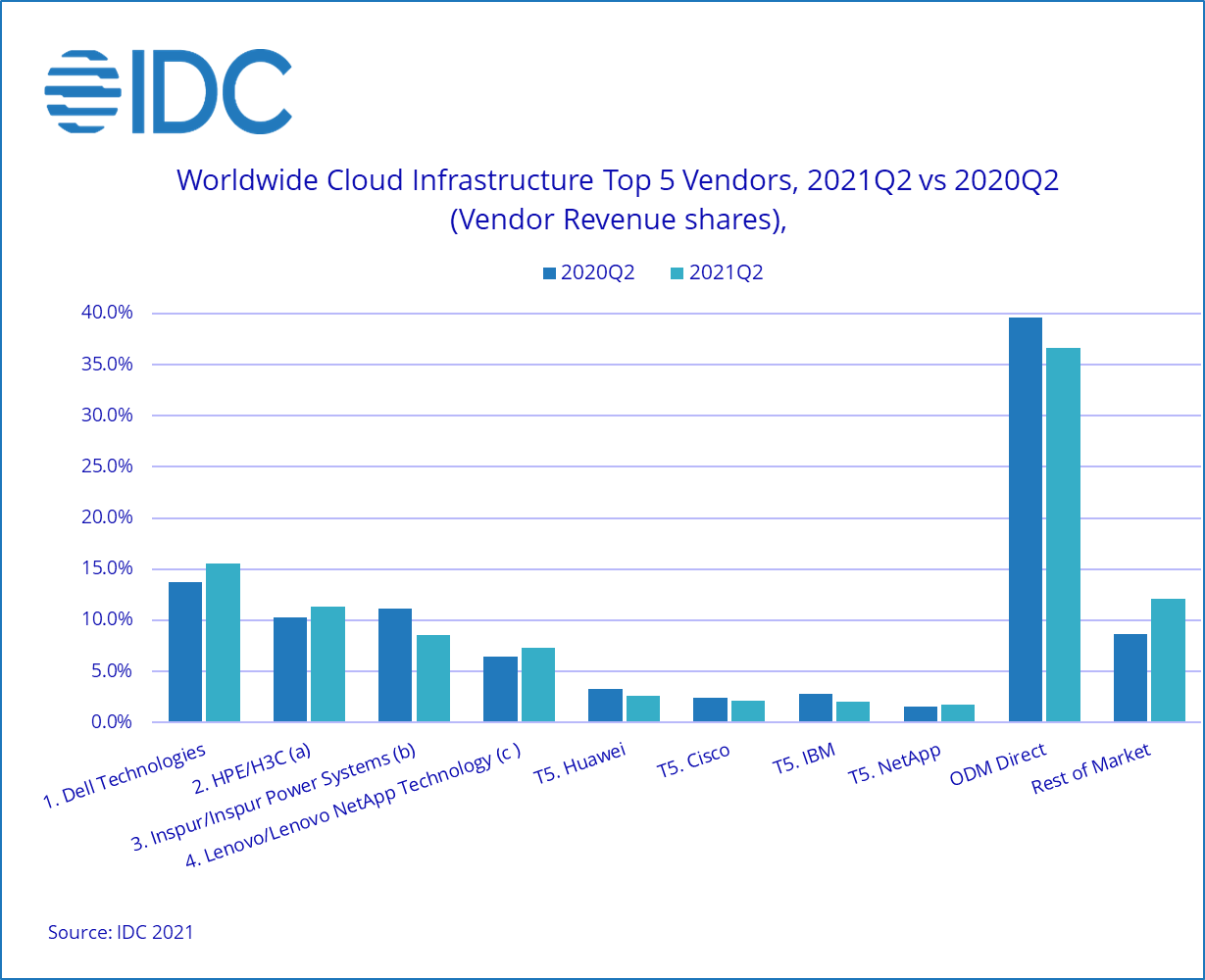

At the company level, major vendors showed mixed results in their cloud infrastructure revenue in Q2/21, with Dell Technologies, HPE/H3C and Lenovo/Lenovo NetApp Technologies increasing sales, while Inspur/Inspur Power Systems and Huawei experienced declines compared with Q2/20.

| Top Companies, Worldwide Cloud Infrastructure Vendor Revenue, Market Share and Year-Over-Year Growth, Q2/21 (Revenues are in Millions) | |||||

| Company | Q2/21 Revenue ($M) | Q2/21 Market Share | Q2/20 Revenue ($M) | Q2/20 Market Share | Q2/21 vs. Q1/20 Revenue Growth |

| 1. Dell Technologies | $2,614 | 15.5% | $2,365 | 13.7% | 10.5% |

| 2. HPE/H3C | $1,911 | 11.4% | $1,773 | 10.3% | 7.8% |

| T3. Inspur/Inspur Power Systems | $1,438 | 8.5% | $1,917 | 11.1% | -25.0% |

| T3. Lenovo/Lenovo NetApp Technologies | $1,225 | 7.3% | $1,107 | 6.4% | 10.6% |

| T5. Huawei | $439 | 2.6% | $573 | 3.3% | -23.4% |

| T5. Cisco | $362 | 2.2% | $423 | 2.5% | -14.4% |

| T5. IBM | $343 | 2% | $491 | 2.8% | -30.2% |

| T5. NetApp | $293 | 1.7% | $263 | 1.5% | 11.3% |

| ODM Direct | $6,166 | 36.7% | $6,832 | 39.6% | -9.8% |

| Rest of Market | $2,033 | 12.1% | $1,492 | 8.7% | 36.2% |

| Total Vendor Revenue | $16,824 | 100% | $17,238 | 100% | -2.4% |

| IDC’s Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, Q2/21 | |||||

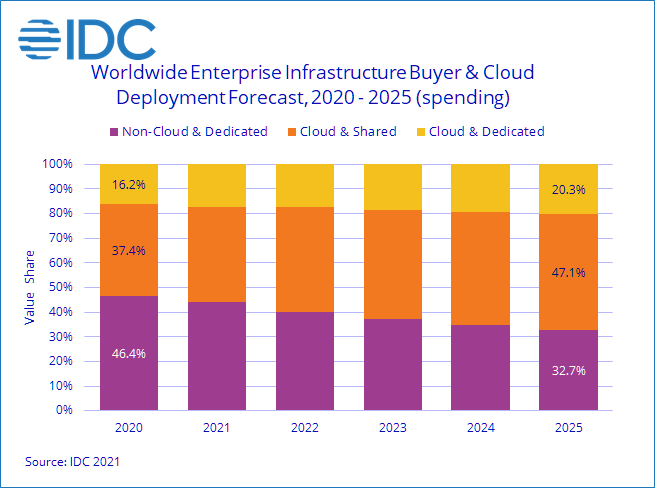

In the long term, IDC expects spending on compute and storage cloud infrastructure to have a compound annual growth rate (CAGR) of 12.4% over the 2020 to 2025 forecast period, reaching $118.8 billion in 2025 and accounting for 67.3% of total compute and storage infrastructure spend. Shared cloud infrastructure will account for 69.9% of this amount, growing at a 12.4% CAGR. Spending on dedicated cloud infrastructure will grow at a CAGR of 12.3%. Spending on non-cloud infrastructure will rebound in 2021 but will flatten out at a CAGR of 0.1%, reaching $57.7 billion in 2025. Spending by service providers on compute and storage infrastructure is expected to grow at an 11.2% CAGR, reaching $115 billion in 2025.

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com