The Financial Accounting Standards Board issued two Accounting Standards Updates (ASUs) that finalize various effective date delays for standards on current expected credit losses (CECL), leases, hedging and long-duration insurance contracts.

The two updates are:

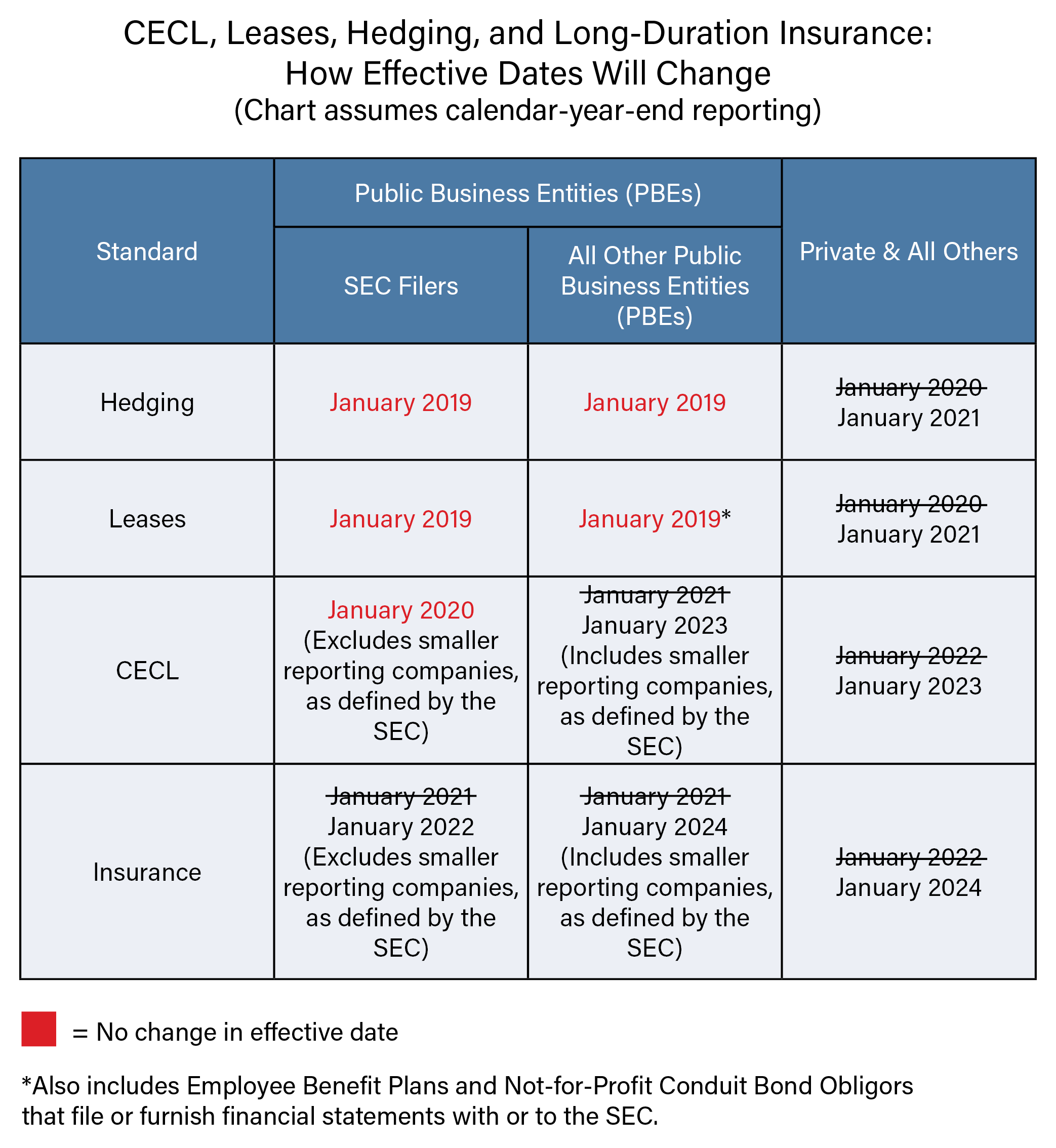

The chart below details all effective date changes:

Both ASUs are available at www.fasb.org.

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com