IT spending expectations remain uneven, with significant differences across countries, industries, and companies, according to the latest update to the IDC COVID-19 Tech Index. Overall sentiment in the U.S. has dropped in the past two weeks, as businesses adjust to bearish GDP forecasts for Q2, and confidence remains soft in Europe. There are tentative signs of improvement in the Asia/Pacific region, however, with confidence levels showing gradual recovery in China and other countries.

Businesses continue to indicate likely cuts to spending on traditional IT products and services in the near term with deep cuts projected by companies that have been directly impacted by the COVID-19 crisis and the resulting economic shutdown. While some firms point towards increased spending on specific technologies, all indicators point towards a significant overall contraction in the next few months with the pace of recovery highly dependent on the pace and stability of measures to reopen economies around the world in Q3.

“A month ago, overall spending projections by IT buyers were still positive in a few areas like artificial intelligence (AI) and other digital transformation projects,” said Stephen Minton, program vice president in IDC’s Customer Insights & Analysis group. “U.S. companies were especially reluctant to impose delays on strategic IT projects and deployments, but the reality of a major economic contraction in Q2 appears to have caught up with CIOs and IT departments in the last few weeks. Where demand is still increasing, it is increasingly focused on a narrow range of technologies that are critical to support remote workers, such as videoconferencing and remote access solutions.”

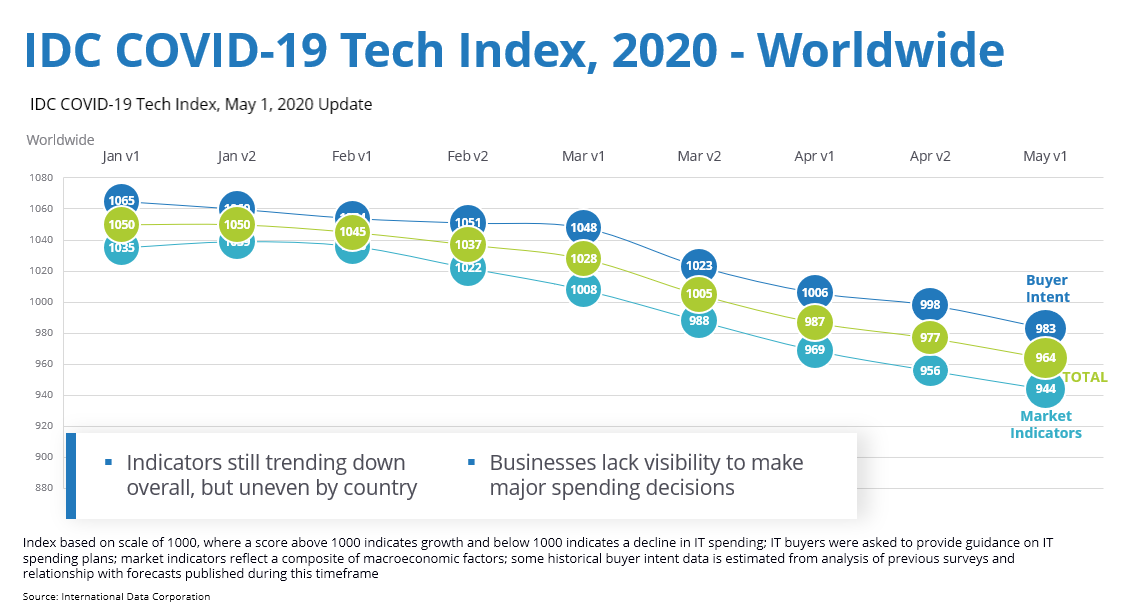

The COVID-19 Tech Index uses a scale of 1000 to provide a directional indicator of changes in the outlook for IT spending and is updated every two weeks. The index is based partly on a global survey of enterprise IT buyers and partly on a composite of market indicators, which are calibrated with country-level analyst inputs relating to medical infection rates, social distancing, travel restrictions, public life and government stimulus. A score above 1000 indicates that IT spending is expected to increase, while a score below 1000 points towards a likely decline.

| COVID-19 Tech Index | March | April | May |

| Buyer Intent | 1023 | 1006 | 983 |

| Market Indicators | 988 | 969 | 944 |

| Total Index | 1005 | 987 | 964 |

| Source: IDC COVID-19 Tech Index, May 2020 (Release 1) | |||

Notes: index score above 1000 indicates expected increase in IT spending for 2020 overall; score below 1000 indicates a projected decline

IT buyer confidence in Europe seemed to stabilize in the first half of April, but then dipped again towards the end of the month. This eb and flow in sentiment is likely to continue for a while as businesses react to uncertainty around the pace, effectiveness, and risks associated with scaling down the restrictive measures that have successfully slowed the spread of the virus but also have led to what most economists believe will be a huge GDP downturn in the current quarter.

“While U.S. and European firms became a little more pessimistic in the second half of April, businesses in Asia/Pacific showed some signs of improving confidence, which reflects a general sense of optimism that the worst may be over in a few countries including China,” said Minton. “The crisis began in China and it makes sense that it may end there soonest, although it’s too soon to be sure this isn’t a false dawn given that measures to open the economy will be carefully managed for any signs of a second wave of infections. The impact on IT spending will be continued uncertainty for some period with many firms lacking the visibility to make major strategic decisions or commit to short-term spending increases.”

Market indicators are still more negative than buyer intent surveys with most economists now extremely pessimistic about the near term while restrictions remain in full force across many countries. Early measures to begin relaxing lockdown measures in some European countries will be watched closely by other countries including the U.S., and any sign of returning strain on health services could lead to a more prolonged period of social distancing. In this uncertain environment, businesses will continue funding mission-critical IT deployments including cloud services and will seek to support remote workers, but some new projects will inevitably be deferred.

“The cloud isn’t going anywhere, all of the data stored in the cloud isn’t going anywhere, and the need for companies to analyze and extract value from all of that information isn’t any less today than it was three months ago,” said Minton. “But decisions to fund new deployments will be hard to make for firms experiencing major declines in revenue and spending cycles will be longer while decision makers are spread around the world in remote locations. New tech products will come to market more slowly and upgrades to office networks or equipment are a low priority while offices remain closed. These headwinds will pass, but there are still milestones to clear before IT spending begins to grow again.”

The IDC COVID-19 Tech Index is a leading indicator for IT spending, which is designed to provide rapid updates to changes in buyer sentiment and underlying market indicators before these are factored into official market and macroeconomic forecasts. The index is based on a scale whereby a score higher than 1000 indicates growth in IT spending, while a score below 1000 indicates a decline. Complete results from the most recent index as well as additional research related to the pandemic can be found on IDC’s COVID-19 microsite.

The index is based on surveys of enterprise IT buyers around the world, who are asked to provide guidance on a variety of factors including general business confidence, overall IT spending plans and specific changes to budget allocations for individual technologies. Additionally, the index score is weighted with a composite of “market indicators” that include macroeconomic forecasts calibrated with inputs relating to medical data, social isolation measures, and the impact of government stimulus.

IDC will host a special COVID-19 Tech Index webinar on May 7 at 11:00 am U.S. EST. In the presentation, Stephen Minton and Jessica Goepfert will discuss the most recent index results, the outlook for technology spending by industry, and how the pandemic is impacting various organizations around the world. Details and registration for this webinar are available here.

Learn how IDC can help your organization anticipate and respond to market changes brought on by the coronavirus pandemic. IDC’s COVID-19 resource site offers research, market data, webinars, and blog articles that can help decision makers plan their next moves in response to the latest developments.

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com