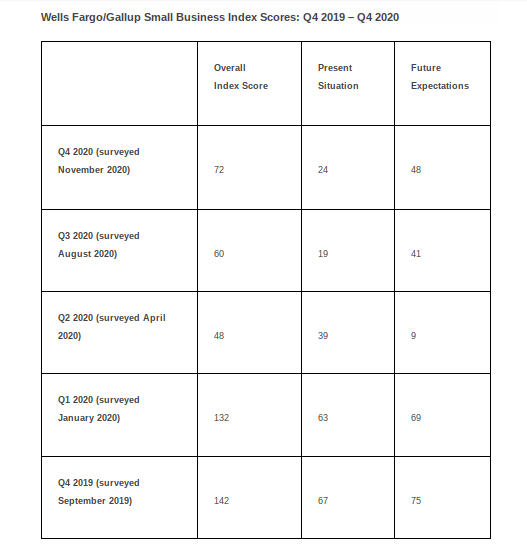

With COVID-19 cases surging and a new wave of restrictions looming, challenges persist for small business owners as they continue to weather the pandemic, according to data from the Q4 Wells Fargo/Gallup Small Business Index. While the index score rose 12 points for the second straight quarter, overall optimism levels remain just above half of what they were in late 2019.

For the third straight quarter, respondents most frequently ranked the loss of business or closings due to the impact of COVID-19 as their top concern. Attracting new business, worries about financial stability and reduced cash flow were the other top ranked concerns.

“With COVID-19 numbers hitting new high-water marks across many states as we enter the important holiday season, small businesses are facing another steep round of challenges,” Steve Troutner, head of small business at Wells Fargo, said. “Helping small businesses keep their doors open, their employees at work and meet their customers’ needs safely is a top priority for Wells Fargo and we are deploying a wide array of tools to do so, including our Open for Business Fund, which is investing approximately $400 million to support small businesses.”

The Q4 survey highlighted that the journey to economic recovery for small businesses will not be a short one. Almost half (46%) of the respondents continued to report decreases in revenue in the last 12 months. The number of owners that felt the economy was growing climbed nine points to 29%, but 33% felt it was continuing to slow, while a combined 38% said it was in a recession or depression.

When asked about the timeline for economic recovery, 28% said it would not come until the second half of 2021, while roughly one third (34%) did not anticipate a recovery until after 2021. More specifically, when asked how long recovery from the impacts of COVID-19 for businesses like theirs would take, more than half (55%) said it would take until the second half of 2021 or beyond.

The pandemic has required many businesses to establish safer ways to engage with customers, including the payments process. Data from the Q4 survey showed that 25% of owners have stopped or reduced their acceptance of cash or check via in-person payment. Credit and debit cards continue to be a staple for online payments (25%) and in person payments (38%). Business owners also have heard that more customers would like the ability to make payments over the phone with a debit or credit card. However, cash and checks remain the largest method of payment, with 74% of businesses continuing to accept them.

“As we think about how to serve our small business customers amid the current COVID environment, it’s critical that we support them with new payment techniques which in turn allow them to operate safely and efficiently,” Liz Ryan, executive vice president and interim head of Wells Fargo Merchant Services, said. “The data tells us that for a large number of business owners, both their current circumstances and their customer preferences are dictating a hygienic approach for payments. As we observe the current shift toward innovative solutions like contactless payments, the pandemic is accelerating the adoption of these capabilities as consumer buying behaviors and preferences change. We continue to operate with a customer-first mindset and focus our support on helping business owners not just survive but thrive.”

Although COVID-19 continues to weigh on small businesses, owners are focused on staying positive and continuing to make thoughtful decisions. Sixty-nine percent of business owners rated their company’s current financial situation as good or somewhat good, and the measure lifted to 73% when asked about 12 months from now. With the shifts and changes small businesses have had to quickly make this year, 46% reported decreases in revenue, but 53% expect revenue to increase over the next 12 months. The survey also indicated that business owners have been very deliberate in their approach to weathering the storm in 2020, with only 23% of owners saying they invested in their businesses this year and only 13% reporting that they added employees. However, for the next 12 months, business owners hope to increase those numbers, with 30% investing in their businesses and 25% adding to their staff.

“Owners seem to be acknowledging the challenges COVID-19 continues to bring to their business, particularly with the resurgence in cases across the country,” Mark Vitner, senior economist with Wells Fargo, said. “With that said, given the myriad of factors that have affected the small business landscape, the continued recovery in optimism indicates these owners see brighter horizons ahead.”

As part of its “Many Hearts. One Community” initiative, Wells Fargo will use its online and social media platforms to shine a light on small businesses and encourage people to shop locally. Additionally, Wells Fargo will deploy approximately $50 million through its Open for Business Fund to nonprofits that help small businesses stay open and to provide relief for small businesses during this time of need.

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com