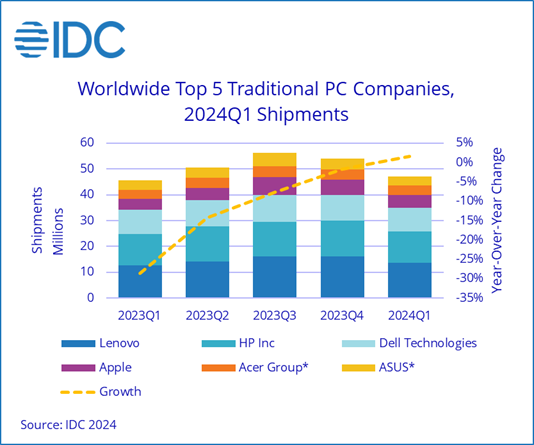

After two years of decline, the worldwide traditional PC market returned to growth during Q1/24 with 59.8 million shipments, growing 1.5% year over year, according to preliminary results from the International Data Corporation’s Worldwide Quarterly Personal Computing Device Tracker. Growth in the market was largely due to easy year-over-year comparisons, as the market declined 28.7% during the first quarter of 2023, which was the lowest point in PC history. In addition, global PC shipments finally returned to pre-pandemic levels, as Q1/24 volumes rivaled those of Q1/19, when 60.5 million units were shipped.

With inflation numbers trending down, PC shipments have begun to recover in most regions, leading to growth in the Americas as well as Europe, the Middle East and Africa (EMEA). However, the deflationary pressures in China have directly impacted the global PC market. Since China is the largest consumer of desktop PCs, weak demand in the country led to yet another quarter of declines for global desktop shipments, which already faced pressure from notebooks as the preferred form factor.

“Despite China’s struggles, the recovery is expected to continue in 2024 as newer AI PCs hit shelves later this year and as commercial buyers begin refreshing the PCs that were purchased during the pandemic,” Jitesh Ubrani, research manager with IDC’s Worldwide Mobile Device Trackers, said. “Along with growth in shipments, AI PCs are also expected to carry higher price tags, providing further opportunity for PC and component makers.”

Among the top five PC manufacturers, Lenovo once again held the top spot and outgrew the market largely due to the steep decline in shipments experienced in Q1/23. Apple’s strong growth was also due to an outsized decline in the prior year.

| Top Five Companies, Worldwide Traditional PC Shipments, Market Share and Year-Over-Year Growth, Q1/24 (Preliminary results, shipments are in millions of units) | |||||

| Company | Q1/24 Shipments | Q1/24 Market Share | Q1/23 Shipments | Q1/23 Market Share | Q1/24-Q1/23 Growth |

| 1. Lenovo | 13.7 | 23% | 12.7 | 21.6% | 7.8% |

| 2. HP | 12 | 20.1% | 12 | 20.4% | 0.2% |

| 3. Dell Technologies | 9.3 | 15.5% | 9.5 | 16.1% | -2.2% |

| 4. Apple | 4.8 | 8.1% | 4.2 | 7.1% | 14.6% |

| 5. Acer Group | 3.7 | 6.2% | 3.4 | 5.7% | 9.2% |

| 5. ASUS | 3.6 | 6.1% | 3.8 | 6.4% | -4.5% |

| Others | 12.6 | 21.1% | 13.3 | 22.6% | -5% |

| Total | 59.8 | 100% | 58.9 | 100% | 1.5% |

| Source: IDC Quarterly Personal Computing Device Tracker, April 8, 2024 | |||||

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com