According to preliminary data from International Data Corporation’s Worldwide Quarterly Mobile Phone Tracker, worldwide smartphone shipments declined 7.8% year over year to 265.3 million units in Q2/23. While this marks the eighth consecutive quarter of contraction as the market struggles with soft demand, inflation, macroeconomic uncertainties and excess inventory, the IDC noted that the rate of decline is slowing compared to previous quarters.

“The good news is that inventory levels are improving and the latest market chatter suggests that by Q3 excess inventory in finished devices and components should clear up,” Nabila Popal, research director for mobility and consumer device trackers at IDC, said. “As inventory levels normalize, we are finally hearing optimism from key OEMs and supply chains and expect the market to return to growth by the end of the year and into 2024. As the market ramps back up, it is also an opportunity for vendors to gain share. IDC expects a shift in the vendor rankings at the bottom of the stack, as we already see happening this quarter with Transsion entering the top five for the first time.”

China experienced a year-over-year decline of 2.1% in Q2/23 after five quarters of significant double-digit contractions. While this is better than past quarters, consumer sentiment and spending remain low. Even the much awaited 618 online shopping festival in June, which was expected to boost sales in China, experienced a 6.5% year-over-year drop in smartphone sales. The Asia/Pacific region (excluding Japan and China), the U.S. and Europe, the Middle East and Africa (EMEA), also experienced shipments declines of 5.9%, 19.1%, and 3.1%, respectively in Q2/23.

“Although the first half of the year has presented many challenges to the market, we believe that there remains plenty of opportunity awaiting in the second half of the year,” Anthony Scarsella, research director for mobile phones at IDC, said. “The foldable market remains an exciting product to consumers, and the arrival of new models and new vendors joining the race will hopefully translate to wider adoption and lower prices. Moreover, we expect the foldable market to grow nearly 50% in 2023 while the total market remains down.”

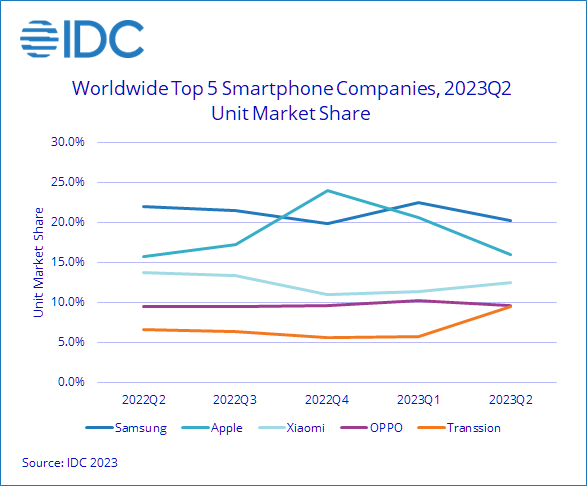

| Top Five Companies, Worldwide Smartphone Shipments, Market Share and Year-Over-Year Growth, Q2/23 (Preliminary results, shipments in millions of units) | |||||

| Company | Q2/23 Shipments | Q2/23 Market Share | Q2/22 Shipments | Q2/22 Market Share | Year-Over-Year Change |

| 1. Samsung | 53.5 | 20.2% | 63.1 | 21.9% | -15.2% |

| 2. Apple | 42.5 | 16% | 45.4 | 15.8% | -6.3% |

| 3. Xiaomi | 33.2 | 12.5% | 39.5 | 13.8% | -16% |

| 4. OPPO | 25.4 | 9.6% | 27.4 | 9.5% | -7.6% |

| 4. Transsion | 25.3 | 9.5% | 18.8 | 6.5% | 34.1% |

| Others | 85.4 | 32.2% | 93.3 | 32.4% | -8.4% |

| Total | 265.3 | 100% | 287.6 | 100% | -7.8% |

| Source: IDC Worldwide Quarterly Mobile Phone Tracker, July 27, 2023 | |||||

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com