Brianna Wilson,

Editor,

Monitor

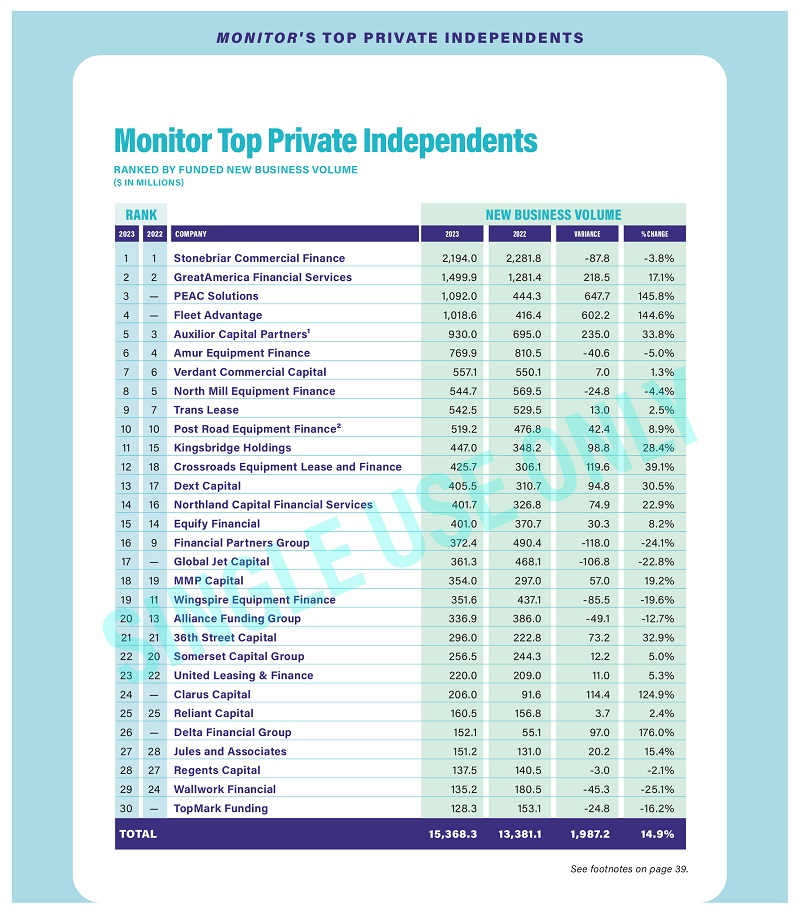

This year, Monitor’s Top 30 Private Independents reported a 14.9% year over-year growth in new business volume — just half of last year’s 30.8% year-over-year growth, which was the second-highest reported in the ranking’s history. Despite the dramatic drop in year-over-year originations, Monitor’s Top 30 Private Independents achieved much more than the 0.53% growth they forecasted for 2023, and they seem far more optimistic about the year ahead.

TOP FIVE

Monitor’s top five independents reported a collective $6,734.5 million in originations, representing 44% of the independents ranking total. With four of the top five companies reporting a year-over-year gain in originations, the top five contributed $1,615.6 (81%) of the top 30’s collective percentage gain.

The top five private independents are familiar, with Stonebriar Commercial Finance maintaining its No. 1 spot, reporting $2,194 million in originations, and GreatAmerica Financial Services similarly maintaining its No. 2 spot, reporting $1,499.9 in total volume. Stonebriar and GreatAmerica alone make up 24% of the group’s total volume.

Stonebriar experienced a $87.8 million (3.8%) drop in originations, down from $2,281.8 million in 2022. Still, the company easily maintains its No. 1 spot in the rankings. With 75% of originations flowing from direct and 25% from indirect channels, Stonebriar continued its focus on primarily large ticket deals in 2023.

GreatAmerica reported a 17.1% increase in new business volume, with 99% of its activity coming from the vendor channel in 2023. GreatAmerica played mainly in the small-ticket arena, though percentage-wise, its micro- and medium-ticket deals weren’t far behind.

After losing its bank affiliation post-acquisition, PEAC Solutions joins the ranking with $1,092 million in volume and Fleet Advantage rejoins the Top 30 with $1,018.6 million in originations after sitting out of the rankings for many years.

PEAC Solutions reported 145.8% year-over-year growth in originations, with 51% of its activity in vendor, 7% indirect, 4% direct and 39% represented by portfolio purchases. PEAC Solutions played mainly in the medium-ticket arena, though its small- and micro-ticket deals flow was not far behind.

Similarly, Fleet Advantage posted a 144.6% year-over-year volume growth, with 100% of originations flowing from its direct channel in 2023. Fleet played solely in the small-ticket arena in 2023.

Auxilior Capital Partners comes in at No. 5 with $930 million in 2023 originations. Auxilior achieved 33.8% year-over-year growth, up from its reported $695 million in new business volume in 2022. Auxilior split its originations evenly between vendor and direct and played primarily in the medium-ticket arena.

TOP PERCENTAGE GAINERS

With a whopping 176% year-over-year volume growth, Delta Financial Group takes the No. 1 spot for top percentage gains. Shortly behind Delta are PEAC Solutions and Fleet Advantage with respective 145.8% and 144.6% year-over-year volume growth. The final “more-than-doubled-your-volume” winner is Clarus Capital with 124.9% year-over-year growth.

NEW ARRIVALS

In addition to PEAC, Monitor welcomed four new companies to the ranking this year: No. 17-ranked Global Jet Capital with $361.3 in originations; No. 24-ranked Clarus Capital with $206 million in originations; No. 26-ranked Delta Financial Group with $152.1 in originations; and No. 30-ranked TopMark Funding with $128.3 in originations.

Delta and Clarus respectively reported 176% and 124.9% year-over-year growth in volume, while TopMark and Global Jet respectively reported 16.2% and 22.8% year-over-year decreases in originations.

Again, Monitor also welcomed Fleet Advantage back into the ranking this year with $1,018.6 million in volume, making a grand return to the Top Independents.

Notably, No. 10-ranked Post Road Equipment Finance is new to the ranking by name only, as the company was formerly known as Encina Equipment Finance.

2023 RETROSPECTIVES

2023 RETROSPECTIVES

Last year, the Top 30 Independents reported margin compression and economy and capital spending as their biggest concerns for 2023. This year, while margin compression remains a top three concern, the economy and capital spending is the top concern, and the independents are also worried about the credit quality of customers.

“The interest rate environment in 2024 resulted in margin compression. Also, bad debt write-offs, aging over 30 days, defaults, NSF’s and repossessions were all up compared to the prior year,” a respondent said. “Industry data was showing aging and default figures the transportation industry hasn’t seen since the Great Recession. Volume was also down significantly year-over-year. There was a lot more competition chasing true A and B credits.”

“The uncertainty in the credit markets, especially after the failures of Signature Bank, Silicon Valley Bank and First Republic, resulted in significant disruption with our funding sources as many pulled to the sidelines during 2023,” another respondent said. “This, combined with the continued rise in interest rates, made it difficult to price transactions and to determine our funding avenues for such transactions.”

Monitor’s Top 30 Independents are also worried about access to quality capital and regulatory constraints heading into 2024.

“The most significant challenge we faced was the continued compression of spreads on new originations,” a respondent said. “The market remained slow to increase yields as there was heightened competition for origination growth and deposit rates at bank competitors were slow to climb. An increase in administrative delinquency as well as state regulations that impacted non-bank financial institutions were also challenges.”

FOCUS IN 2024

Many top independents plan to focus on growing their originations in 2024.

“We want to continue to grow at a steady pace,” a respondent said. “Making sure training, processes and most of all customer service stays our top priority is the biggest challenge of growth.”

Speaking directly to volume growth, a respondent said, “Increasing new volume for 2024 is a key focus of ours. Adding new customers while retaining our good ones is very important. By adding new folks to our sales team in areas of the country where we see a lot of opportunity and streamlining our process for developing leads, we feel confident that we can increase our volume year over year by 5%.”

One company plans to “develop a new origination channel for the business.”

Several companies also expect to implement new technology or improve existing technology as the industry continues shifting into a digital-forward world.

“The future requires a more digitally-enabled and, in some cases, automated experience for customers and team members,” a respondent said.

Speaking to opportunity, another respondent said, “We plan to expand relationships by seeking to be better and continuing to fill the voids created where banks have pulled back.”

2024 FORECAST

Despite the somewhat rough year and challenges that lay ahead, Monitor’s Top Private Independents are optimistic about the opportunities in 2024. Compared to its 0.53% growth prediction last year, the independents predicted a collective year-over-year growth of 22.14% in new business volume, which would result in a year-over-year a dollar gain of $3,402.3 million. Though a few companies do expect no growth in 2024, no companies predicted a decrease in originations. The Top Independents have made rapid progression since the 9.1% year-over-year originations increase in the wake of the COVID-19 pandemic.

SUMMARY

Overall, the independents had a decent year with only 10 companies reporting a decrease in year-over-year originations growth from 2022 to 2023. With only a few companies reporting more than a 20% decrease in originations, no single company took a massive hit to their year-over-year new business volume.

The independents reported a nearly-even split between direct originations (43% of total deals) and vendor channel activity (40% of total deals), with direct coming in at $6,578.8, up from $5,830.5 million in 2022, and vendor coming in at $6,107.2 million, up from $5,514.1 million in 2022. The next largest origination channel was indirect, coming in at $1,872.6 million, up 12% from $1,682.8 million in 2022.

In terms of employee productivity, with a collective 3,025 employees across all companies, the Top Private Independents reported an average of $5.26 million in volume per employee, a slight drop from the $5.55 million per employee reported in 2022.

After two record-breaking growth years in a row, the independents experienced a dip in originations in 2023. However, despite the challenges and the concerns for the remainder of the year, Monitor’s Top Private Independents are feeling optimistic, predicting a 22.14% gain in new business volume.

Monitor’s staff is grateful to the companies that participate in our annual survey and make this report possible. •

ABOUT THE SURVEY:BASIS FOR RANKING

To meet the criteria for selection, companies that qualify must be privately owned with equity provided by the individual owners and/or privately held owners. Participants were asked to provide full-year data relating to funded new business volume, which was to include information pertaining to equipment-related loans and leases only.

We also collected information such as staffing levels, origination and funding sources, average deal size, etc. Once received, the data was compiled, checked for accuracy and formatted for this report.

A company’s position in the Monitor’s Top Private Independents ranking is based solely on its funded new business volume.

Questions/Participation Inquiries: Please contact Rita Garwood at [email protected].

No categories available

No tags available