With shipments totaling 68.5 million units in the third quarter of 2023, the global PC market managed to outperform expectations. However, that volume was still down 7.2% compared to the same quarter in 2022, according to the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker.

Despite the PC market surpassing initial forecasts, both driving and inhibiting factors influenced this performance. First, the increased volume can partly be attributed to inventory restocking, mostly on the consumer side. Second, there was a notable effort to address anticipated cost escalations, such as expected increases in India import duties. Although these duties were later suspended, such concerns nonetheless led to the channel absorbing more units than likely necessary. Finally, further tightened IT budgets led business PC units to underperform against an already conservative commercial forecast.

Given current conditions and a tenuous macroeconomic environment, IDC has lowered its forecast for the worldwide PC market. 2023 shipment volume is now expected to decline 13.8% compared to 2022, which itself declined 16.6% over the previous year. Two consecutive years of double-digit year-over-year drops is an unprecedented trend in the PC market but will likely contribute to a recovery thereafter. Despite the short-term challenges, IDC continues to expect a market rebound in 2024 and beyond with many factors converging within the next two years. A few of the main drivers include:

The collective influence of these factors positions 2024 as a pivotal year for the PC market, offering a respite from recent challenges. Beyond 2024, growth is expected to surpass pre-pandemic shipment levels and culminate in 285 million units by 2027.

“Perhaps historical context can offer some consolation to the tough slog the PC ecosystem is going through,” Jay Chou, research manager for IDC Mobility and Consumer Device Trackers, said. “While we still expect eight consecutive quarters of year-over-year volume declines from Q1/2022 through Q4/2023, it still pales to the 19 consecutive quarters of year-over-year PC declines from Q2/2012 to Q4/2016. Furthermore, notebooks are already at higher levels than 2019, signaling a sizable expansion of the notebook market even after COVID-induced purchases have subsided. We maintain that factors like hybrid work, commercial refresh and growth in premium PCs can lead to a compound annual growth rate of 3.1% from 2023 through 2027.”

| Worldwide Personal Computing Device Forecast by Market Segment: Shipments, Year-Over-Year Growth, and 2023-2027 CAGR (shipments in millions) | |||||

| Segment | 2023 Shipments | 2023/2022 Growth | 2027 Shipments | 2027/2026 Growth | 2023-2027 CAGR |

| Consumer | 113.9 | -14.8% | 125.5 | 1.4% | 2.4% |

| Education | 29.6 | -15.4% | 35.0 | 0.8% | 4.2% |

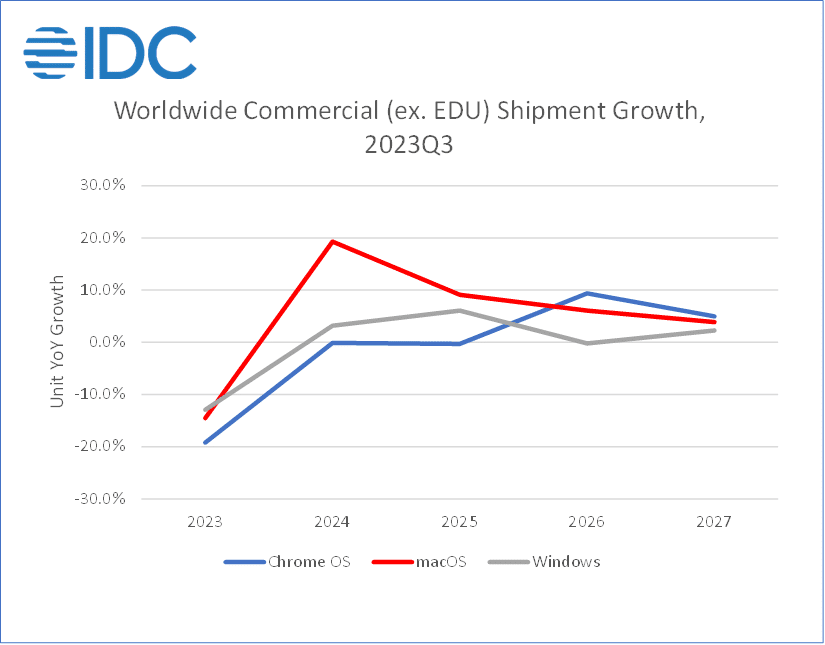

| Commercial (ex. Edu) | 108.3 | -12.2% | 124.6 | 2.6% | 3.6% |

| Total | 251.8 | -13.8% | 285.0 | 1.8% | 3.1% |

| Source: IDC Worldwide Personal Computing Device Tracker, December 21, 2023 | |||||

Notes:

IDC’s Worldwide Quarterly Personal Computing Device Tracker gathers detailed market data in over 90 countries. The research includes historical and forecast trend analysis among other data. For more information, or to subscribe to the research, contact Jackie Kliem at 508-988-7984 or [email protected].

Like this story? Begin each business day with news you need to know! Click here to register now for our FREE Daily E-News Broadcast and start YOUR day informed!

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com