Jody Green is the president of Commerce Bank Equipment Finance.

Jody Green is the president of Commerce Bank Equipment Finance.

Liability policies are standard procedure when leasing equipment, but not all policies will cover vicarious liability in the event of an accident caused by the lessee or require the same financial responsibility depending on the state. Jody Green and Bill Mulder provide a basic breakdown of when additional insurance may be necessary and the types of equipment that most need its protection.

All financial institutions have a liability policy, and most believe the policy covers vicarious liability arising from leased assets. For example, as a lessor, you lease a motor vehicle which is involved in an accident caused by the lessee. The general rule is that the lessor’s liability policy does not cover vicarious liability relating to leased assets. If you believe your policy does cover this event, you may want to contact your insurance broker to verify it. Most companies are unaware of this lack of coverage and have not purchased separate ‘contingent’ uninsured or ‘excess’ underinsured liability insurance to cover this gap.

The next issue is whether you need to purchase contingent liability insurance and, if so, determine which assets it makes economic sense to cover. For example, if you are a general lessor, you may not want to purchase contingent liability insurance for some equipment types (furniture and fixtures, IT equipment) or for some customers (those with higher net worth or higher credit standards, such as publicly held companies) or based upon applicable laws in effect.

Finally, it is called contingent liability insurance because in the vast majority of circumstances, your lessee is required to obtain their own insurance liability policy. which lists your company as added insured. The contingent insurance becomes active if the lessee’s insurance is not in place, is insufficient in amount or does not cover the event. Whether contingent liability insurance should be obtained and in what amount should be based upon your own follow up on insurance renewal certificates and the credit and insurance default rate of your portfolio .

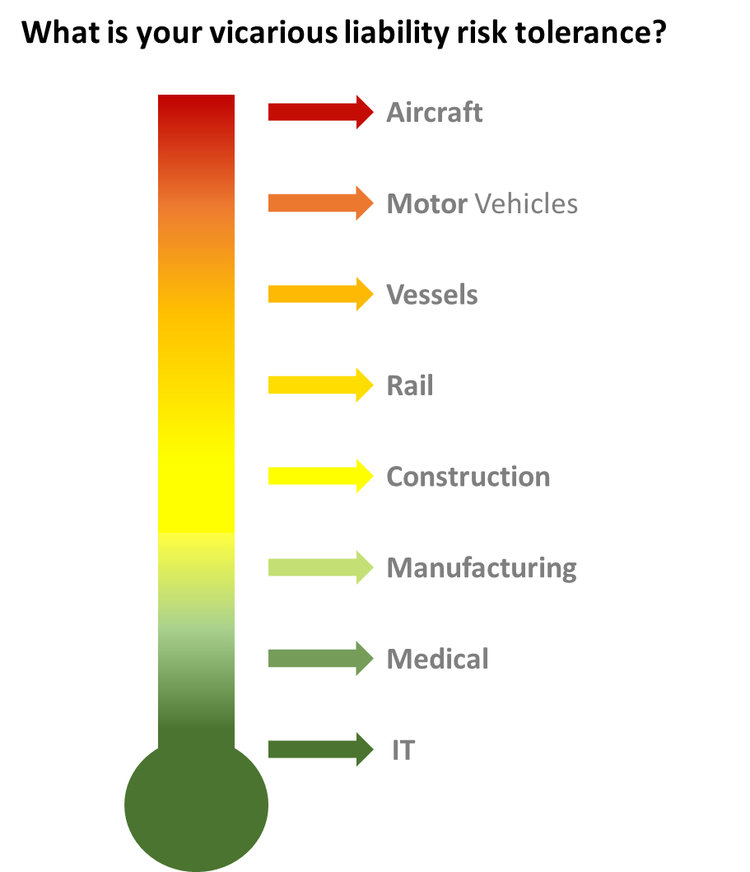

To decide the optimal amount and type of insurance needed, you should evaluate the potential for vicarious liability, which is best discussed with your insurance broker and counsel. Examples of current statutes limiting lessor vicarious liability and mitigating the need for contingent vicarious liability insurance follow.

Aircraft

49 U.S.C. 44112 addresses limitations of liability for parties with interests in aircraft. It states, in part, “A lessor, owner, or secured party is liable for personal injury, death, or property loss or damage … only when a civil aircraft, aircraft engine, or propeller is in the actual possession or control of the lessor, owner, or secured party, and the personal injury … because of (1) the aircraft, engine, or propeller.”

The primary insurance coverage is the lessee’s own liability policy, but with judgment amounts on the rise, what was an acceptable amount a few years ago may be insufficient now. Today, minimum requirements may reach $100 million for corporate jets and $300 million for specialty aircraft.

Although the federal statute should preempt state law, some state court cases have determined additional liability for financiers of aircraft and prompted some aircraft lessors to obtain additional vicarious liability insurance coverage.

In response to these and other cases, the federal statute was modified by the FAA Reauthorization Act of 2018, part of which is intended to further limit vicarious liability of non-active lessors. We have yet to see the effect of the new law on vicarious liability claims.

Motor Vehicles

The Graves Amendment, which was codified as 49 U.S.C. 30106, limits vicarious liability for non-active lessors of motor vehicles. This 2005 federal law, however, did not preempt state statues which impose financial responsibility on “the owner of a motor vehicle for the privilege of registering and operating a motor vehicle or … on business entities engaged in the trade or business of renting or leasing motor vehicles.”

The financial responsibility laws were enacted to ensure an injured victim received some compensation. These laws generally create primary liability on the owner of the motor vehicle for the acts of the operator, based on the theory that if A owns a car and lends or leases it to B, who doesn’t own a car and doesn’t have insurance; and B causes an accident that injures C; C can recover from A, who is required to have insurance on his own car. The Graves Amendment stipulates that if A is listed as owner on the title of a vehicle which is involved in an accident, A will generally not be held liable for vicarious liability caused by operator B, but A will be required to pay the minimum financial responsibility amount, which varies by state, but is generally between $25,000 and $50,000 per event.

Our experience has been that accidents are usually not caused by operators of fleets or larger Class 8 type trucks, as drivers are generally well-trained and heavily regulated by federal law. Additionally, electronic logs are now required to ensure drivers are well-rested and well-trained to obtain and retain the commercial driver’s license required to drive most Class 8 trucks. Operators who are not well-trained, such as short-term lessees of rental moving vehicles or employees driving delivery trucks, are more likely to be involved in accidents.

Marine

For brevity, this discussion is limited to vessels in U.S. waters. Unlike aircraft and motor vehicles, there is no federal statute designed to eliminate vicarious liability. Due to this lack of explicit regulation, the need for insurance is increased. The need for contingent vicarious liability insurance, however, is mitigated, as vessels and barges tend not to hit something that causes damage. Additionally, most operators and crews are experienced and are subject to significant federal regulations similar to the trucking industry regarding subjects such as maximum work hours and minimum sleep time.

For marine vehicles, note that pollution insurance may be of equal or more importance than general liability insurance, as pollution damage is generally not covered by the lessee’s general liability insurance nor with a lessor’s contingent vicarious liability policy.

Rail Equipment

The rail industry is similar to the marine and trucking industries, as there is substantial federal regulation of the operators to limit on-duty time. The major factor mitigating vicarious liability in rail transactions is that owners of the tracks, such as Union Pacific or BNSF, are primarily responsible for the accidents, as they operate the trains and maintain the track. The second responsible party is typically the lessee of the rail car. This responsibility is taken on through indemnification provisions in the lease agreement and covered by their insurance policy. Although there is no federal statute for rail limiting vicarious liability similar to those for aircraft and motor vehicles, there are generally a few layers of liability which must be exhausted before a lessor may be required to pay a judgment related to vicarious liability.

General Thoughts

Some financial institutions have tried to reduce vicarious liability by placing assets in separate subsidiary limited liability companies. This approach is not always successful, as plaintiffs attempt to “pierce the corporate veil,” which can result in the parent company being liable.

Another approach is to place assets in a subsidiary entity with little equity due to loans to the subsidiary for its leasing portfolio. As in the example above, some plaintiffs have been successful in piercing the corporate veil, which can result in liability for the parent company. Other theories include subordinating the subsidiary’s debt to parent to that of the claims of injured parties.

Some financial institutions believe when they purchase leases from another entity and leave the titles for motor vehicles in the other entities’ name pursuant to a titling trust, the trust will protect them. However, most such trusts are created to reduce the cost of re-titling the vehicles in the new lessor’s name and place the liability on the entity that purchased the leases through indemnification provisions. There are some titling trusts designed to limit vicarious liability, but they encounter the same issues encountered by creating separate entities to place leased assets.

The more prudent approach to limit vicarious liability is to purchase only what you need when buying contingency insurance. Consider your internal policies on insurance as a requirement of funding and procedures for your people and their follow up for renewal certificates. Do you have good and effective policies and obtain proof of the lessee’s liability insurance prior to funding? How good is your follow up for insurance certificates? If you are not aware of what percentage of your portfolio has expired insurance and you have not obtained a renewal certificate, you may want to consider buying some or more contingent liability insurance.

The next factor to consider is what part of the portfolio most needs vicarious liability insurance. Some equipment types or credit levels may not warrant the cost of insurance.

Conclusion

The first line of defense is to invest in your own people. Have them track renewal insurance certificates and make insurance tracking an objective goal for performance reviews. It may take a couple years to work up to high levels of compliance for renewal certificates, but maximized insurance coverage is achievable (without force-placed insurance). Stratify your risk. Assets that move are higher risk, while non-moving assets have lower risk profiles. Finally, stratify your customers. If a customer is on your watch list, they must have insurance.

Engage your employees by having your insurance broker teach them how to read the various Acord certificates. Your broker is receiving your premiums and should provide this training free of charge. They can be the best qualified training source.

Bring legal counsel in for a ‘lunch-time learning’ to talk to all employees about examples of vicarious liability and the importance of tracking renewal insurance certificates. Insurance tracking may appear to be a tedious job with no real importance, but employees often like a free lunch, appreciate learning about the importance of their job, and interacting with counsel. Most counsel will provide this session at little to no cost.

Finally, talk with your insurance broker and legal counsel to determine the optimal level of insurance coverage for each type of equipment.

This article is provided as general principles, not as legal advice. Speak with your legal counsel about your specific portfolio and what is best for you. •

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com