Patricia Voorhees is a director of The Alta Group in the Management Consulting and Merger and Acquisition Advisory Practices. She has more than 25 years’ experience in technology and commercial finance. Her areas of expertise include B2B fintech, vendor/captive leasing, mergers and acquisitions, small-ticket leasing and pricing. Voorhees is a frequent author and speaker on fintech in asset finance and serves on the steering committee for the Commercial Equipment Marketplace Council.

Patricia Voorhees is a director of The Alta Group in the Management Consulting and Merger and Acquisition Advisory Practices. She has more than 25 years’ experience in technology and commercial finance. Her areas of expertise include B2B fintech, vendor/captive leasing, mergers and acquisitions, small-ticket leasing and pricing. Voorhees is a frequent author and speaker on fintech in asset finance and serves on the steering committee for the Commercial Equipment Marketplace Council.

Fintech Gen 1 may have smoothed out processes on the back-end of equipment finance, but its successors may prove to be truly disruptive on the front-end. Patricia Voorhees examines the ways fintech may come to define and change the customer experience.

Financial technology — fintech — has reshaped the financing landscape for more than a decade. How has this first generation of fintech transformed equipment finance? How will the next? Turns out Fintech Gen 1 has proven more of an industry influencer than a true disrupter. Some traditional players have invested in this technology, and some fintech lenders have expanded their footprints in equipment finance. Either way, fintech has certainly helped improve customer acquisition and access to credit, particularly with small and mid-sized business (SMB) customers.

Although fintech SMB lenders have not had a fundamentally disruptive effect on the equipment finance space, they are clearly gaining share very quickly; the top five did a combined $11 billion in 2018 originations. They are also keenly focused on customer needs, adding financial products and honing their customer experience.

However, we’re now entering Fintech Gen 2. which has the potential to be much more disruptive for equipment finance.

Where Gen 1 focused on online models for efficiency in customer acquisition and underwriting, Gen 2 is driven by business customers’ demand for a consumer-like online buying experience, including integrated access to the full spectrum of payment choices and equipment access models. This is where the “tech” part of fintech begins to take the driver’s seat to satisfy this user-driven demand. Two areas we will explore are technology that delivers consumer-like, e-commerce experiences, coupled with full payments and financing; and new models of acquisition powered by big data and predictive analytics.

B2B Wants B2C Experiences

The scale of B2B e-commerce has reached a tipping point because online B2B commerce now exceeds traditional B2B commerce. Forrester Research data estimates that it surpassed $800 billion in 2018 and grew 9.8% from 2012 to 2018, compared with $540 billion and a 1.5% growth rate for offline B2B. By 2021, B2B e-commerce is expected to exceed $1 trillion.

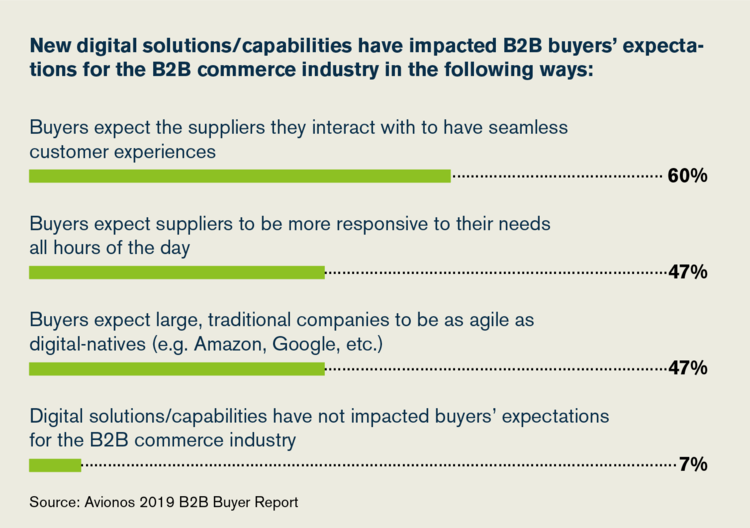

A rising demand for simple, Amazon-like buying experiences has accompanied the growth of B2B e-commerce. Based on work The Alta Group has done over the past year, it is clear that SMB customers find the simplest aspects of equipment acquisition to be frustrating. The top three complaints were: where to find product comparisons, how to purchase products and how to pay for them. Another source of significant frustration was the overall time from the realization of an equipment need to the delivery of said critical equipment.

So, what do B2B equipment buyers expect? A process that is simple and seamless regardless of the ticket size of the transaction. In fact, they expect their suppliers to offer a process as agile as digital natives Google and Amazon provide. This includes the ability to access product videos and comparison tools for product selection and, while preserving the integrity of the shopping cart, move on to options for payment. As original equipment manufacturers (OEMs) utilize video and virtual artificial-intelligence (AI) driven shopping experiences, they are raising the bar for their equipment finance partners in understanding buyer decision journeys and the need for payment and financing at point of sale (POS).

Players entrenched in the payments space, such as Square, are leveraging their place in the SMB check-out process to drive loan volume at virtually zero incremental customer acquisition cost. Square, which has grown volume 16 times since 2014, offers SMB customers loans to expand their businesses. Amazon offers qualified sellers loans from $1,000 to $750,000. Repayments are deducted from the seller’s Amazon account, and any losses are covered by sales proceeds or by seizing seller inventory in company warehouses. Currency, a fintech steeped in the equipment finance space, has launched CurrencyPay to add payments capability along with leasing at POS. OnDeck is expanding its equipment finance product, announced late last year, to satisfy demand from its SMB customer base.

This demand for a better user experience is not limited to SMB customers. Models are beginning to emerge in the equipment finance space that promise to allow financing of big-ticket items online. Innovation Finance, a fintech equipment finance company, is approaching the market through a smartphone enabled app — QuickFi. The company is utilizing biometric authentication AI and blockchain to create an easy, transparent and seamless experience for borrowers from investment grade to SMB, regardless of ticket size, and all of it right from their mobile phones.

User demand for technology enabled, optimized equipment buying combined with seamless online payment is likely to continue to grow. Equipment finance players that focus on the customer journey and provide an optimal experience, on their own or via partnerships, will be well positioned for the future.

New Equipment Acquisition and Risk Models Emerging

Companies are also leveraging fintech for exciting, new equipment acquisition models and risk frameworks. An example is Fair, whose CEO Scott Painter spoke at the Commercial Equipment Marketplace Council (CEMC) 2019 Fintech Innovation Summit. Painter discussed how he turned the risk, pricing and usage model on its head to deliver a solution. The problem Painter set out to solve with Fair is that the average vehicle purchase price equals 30% of the buyer’s net worth. Most buyers finance their vehicles, adding to their debt burden while acquiring an asset with its steepest depreciation in the first couple of years of ownership.

Fair focused on providing a mobility contract via a smartphone-based app where users can search used car inventories at local dealerships. Painter shifted the pricing and risk model by focusing only on offering cars past the first two-year depreciation curve. The company certainly does a traditional credit pull, but it is anticipating the consumer will likely steal the vehicle (0.5% have to date), since they are only signing up for a cancelable, month-to-month contract.

Its asset risk model utilizes big data and predictive analytics, which build with each new customer to deliver what Painter called “radical clarity about the value of the vehicle.” Unlike traditional auto leasing, it isn’t determining the asset value at the end of lease. The company is using big data and predictive analytics to understand the value of a particular vehicle on a particular day. Certainly, the availability of VIN numbers-based individual automobile level data gives the titled vehicle space a head start, but data-driven new acquisition models are emerging in other asset classes.

Another great example is EquipmentShare, a peer-to-peer construction equipment company that emerged four years ago. It was founded by contractors to solve two particular problems: access to equipment where and as needed and the underutilization of contractor-owned construction equipment. The company has grown quickly to 27 full-service locations in 11 states and two countries. What makes the model interesting in terms of enabling new equipment acquisition models is the technology.

The rental aspect of the EquipmentShare value proposition satisfies a critical need, but it is its telematics-based Track product that offers promise in enabling new equipment acquisition models. The product provides a mixed fleet solution for vehicles and equipment. Through the advanced telematics technology, equipment owners can control their assets and provide access to them. The functionality of Track includes GPS, geofencing to set physical boundaries, digital work orders, equipment usage reports and driver scorecards.

The power comes into play by combining the rental, ownership and tracking aspect of EquipmentShare. With the technology to manage the equipment, more contractors can opt to become fleet owners and drive asset return. Models like EquipmentShare also can offer equipment vendors and finance companies the ability to provide usage-based financing while minimizing asset risk.

eTrack Tech is another example of a fintech-fueled business model. Its CEO, Barbara Timm-Brock, also spoke at the CEMC event. eTrack is a startup focused on mixed fleet management in the material handling space. Its mission is to optimize forklift safety and uptime by managing predictive maintenance and utilization. The product utilizes internet of things (IoT) enabled predictive insights to help managers of facilities, distribution and logistics eliminate downtime and improve safety and productivity while saving money on repairs and maintenance. Although the company is a startup, the technology offers promise to material handling equipment owners and finance companies interested in usage-based finance products and optimizing asset life and returns.

Conclusion

The first generation of fintech made its mark on customer acquisition and underwriting in equipment finance. Now Fintech Gen 2 is changing buyer expectations, acquisition models and risk frameworks. It is poised to become a true industry disrupter as B2B e-commerce continues to grow.

Equipment finance players that want to stay relevant must invest in fintech strategically for their businesses. One key area where they should focus their efforts is using fintech to satisfy the demand for better online buying experiences and usage-based financing options. •

Terry Mulreany

Subscriptions: 800 708 9373 x130

[email protected]

Susie Angelucci

Advertising: 484.459.3016

[email protected]

Visit our sister website for news, information, exclusive articles,

deal tables and more on the asset-based lending, factoring,

and restructuring industries.

www.abfjournal.com